Planning for a property purchase as a US person in the UK

Partner and Head of Advanced Planning at MASECO private wealth, Andrea Solana examines the historical challenges and changes for U.S. citizens to purchase property in the U.K., and how to best navigate the current landscape.

Historically, property alongside pensions have been one of the most common ways to invest in the UK both for a main residence and a buy-to-let portfolio. As many know, property is an asset class, just as cash, bonds and shares and can serve as a form of diversification when building an overall investment portfolio for assets. In the UK, there have traditionally been many tax incentives for property investing. However, these are slowly being tapered back making other avenues of investing potentially more attractive. Below we will explore some of the important financial considerations with respect to owning property. Why has investing in UK property been historically attractive? The UK does not currently charge capital gains tax on the sale of a main residence. As property prices have increased over the years, it has allowed individuals to upgrade and downsize their properties and keep their gains intact without the extra consideration of what might be payable to HMRC. In addition to tax advantages provided for a main residence, the UK also allowed for attractive benefits related to buy-to-let properties. Landlords buy to let properties have been able to generate considerable rental income and that income could be offset against mortgage interest and other ‘wear and tear’ allowances leaving a very tax efficient way to place capital to work.

What has changed?

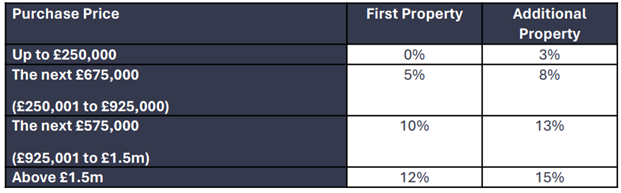

Beginning in April 2016, second properties now attract an additional 3% Stamp Duty Land Tax (SDLT) charge on purchase. The comparative rates applying for SDLT on residential property in England and Northern Ireland, on transactions with effective dates (normally the completion date) from 23 September 2022 to 31 March 2025, are outlined below:

Upon sale of a second property, UK capital gains tax is charged at 28% (assuming you are a higher rate or additional rate taxpayer) as opposed to a more favourable gains tax of 20% for the sale of other investments such as shares.

Additionally, over the next few years, mortgage interest relief is supposed to be capped at a 20% basic rate of tax benefit and gross rental income will be used to determine the tax rate applicable on the net rental income earned each year. With some of the incentives being tapered back, many people are reconsidering its place in their overall investment portfolio.

The traditional financial considerations of a home purchase in the UK

When it comes to planning for a home purchase in the UK, the traditional factors and aspects of your financial life to consider include:

How much can I (and should I) put down?

When considering how much to put down on a home purchase, you need to think about what you have in the way of existing liquid assets versus what you will pay off over time. The more you put down up front the more equity you are putting into the property as you move forward. Frequently, the larger the deposit, the greater the choice of mortgage deals. The exact amount of deposit will depend on individual facts and circumstances.

Have I taken into account any Stamp Duty Land Tax (SDLT) and Conveyancing Fees that will be payable?

It is easy to forget about how much SDLT and Conveyancing Fees amount to when you are purchasing a property. When looking at how much you have available to allocate towards a deposit you also need to consider the cash outlay for these.

What kind of mortgage do I want to secure?

Knowing whether it is beneficial to secure an interest only loan or a principal repayment mortgage as well as looking at the appropriate repayment period and repayment vehicle are all important things to understand and give consideration to. Additionally, you want to think about whether you want a fixed rate or variable rate and what, if any, associated insurance protections are appropriate. The decisions made here will first and foremost impact monthly cash flow. Thinking through how the property will be used now and in the future and knowing how long you may own the property are factors to take into account.

What can property offer investors?

As noted above, property is an asset class separate and distinct from fixed income and equities. Therefore, it can serve as a diversifier within an individual’s overall investment portfolio. When you own property, there are two main ways to earn a return:

- Make the property a buy-to-let and earn an income stream over time by letting it out to tenants.

- Hold the property for use as a main residence or second home and sell the property at a later date for a higher price than you purchased it for.

For some approaching retirement, a buy-to-let property may, depending on individual circumstances, offer an income stream to supplement pension income and possibly serve as a form of annuity over time.

What are the risks of investing in property?

It may not seem like it from recent history, but it is important to remember that property prices and demand for rentals can ebb and flow over time. Additionally, property is considered to be a more illiquid investment as you cannot get your money out immediately if you need quick access to capital. There is also the spectre of negative equity if property values fall significantly and the mortgage is higher than the value when you want to move/sell!

It is important to factor in any buying, selling, maintenance and management costs associated with owning a property, as these are not insignificant. Additionally, this not only involves financial costs but also a time cost. When there is a mortgage in place, you need to factor in that there is no guarantee that the rental income will fully cover the loan repayment over time. And, if you cannot keep up with the loan repayments, the bank can reclaim the property. This is why it is important to remember that investment in property should be a longterm buying decision and time horizon and access to other more liquid sources of capital should be carefully considered before purchase. If the housing market slows down, having the ability to postpone a sale until more favourable market conditions return will help increase the odds of a profitable investment

The additional considerations of UK property purchase for an American

As with other financial decisions, Americans often have additional areas of consideration.

At purchase, Americans need to assess their sources of capital for a deposit. If any assets will be brought onshore from the US or other locations outside of the UK, it is important to understand whether those assets are considered ‘clean’ from a remittance standpoint or whether there will be a tax charge in the UK upon bringing that money in. Understanding any tax charges that might be applicable is extremely important as no one wants to be surprised to find out that a chunk of the assets available to put towards a deposit is actually going to go towards paying a UK tax bill.

When an American is married to a non-American, there is an additional consideration relating to the appropriate ownership structure. The sale of a main residence has tax implications for an American individual whereas, as noted earlier, it is tax free from a UK perspective. When one spouse is not American, it can often be beneficial to think about the ownership structure of the property and determine whether it is in the family interest to consider joint tenants in common or ownership in the non-US spouse’s name. The amount a mortgage lender will lend will also be based on who is going to own the property.

At sale, in addition, to understanding whether the property qualifies as the individual’s principal residence under certain IRS definitions entitling them to receive a $250,000 gain exclusion on the sale before any US tax applies, the fluctuation of foreign currency exchange rates can have a large impact on the recognition of gains upon disposal of real property. The exchange rate on the date of purchase and the date of sale are used to determine the taxable gain in local currency.

When a mortgage is paid off on a foreign property, the owner also must calculate whether there has been a gain or loss on the disposition of the mortgage due to exchange rate fluctuations. If a mortgage costs less at settlement due to the exchange rate at sale and the date the mortgage was obtained, the portion of gain recognised on the mortgage repayment is taxed at ordinary income tax rates. Without careful consideration of the currency fluctuation over the period of ownership, a taxpayer can sometimes unknowingly create large gains in local currency.

Planning well ahead of a property purchase will help ensure that you’ve given proper consideration to the above and will help ensure that you don’t get adversely surprised as you embark on a very large financial purchase.

About the Author

Andrea Solana is Head of Advanced Planning at MASECO Private Wealth where she helps to provide financial planning and wealth structuring advisory services to US expatriates in the UK and British nationals in the US. Before joining MASECO, Andrea spent the first part of her career with a well-known Washington DC based international tax and global wealth management firm where she gained considerable experience advising high net worth individuals with multi-jurisdictional financial interests to design and implement strategies for tax-efficient and risk-managed asset growth. She has written numerous white papers regarding fundamental financial planning and investment strategies for U.S. connected individuals and has previously been a speaker on financial planning topics at numerous places including both The World Bank and International Monetary Fund (IMF). Andrea graduated from University of Virginia’s McIntire School of Commerce with a degree in Finance and Management and completed her MBA at Imperial College London.

The importance of retirement planning for female investors

Mind the pension gap! Wealth Manager at MASECO Private Wealth Emma James discusses the daunting task of financial planning for the future and its importance, especially for women.