Digital Assets and Private Placement Life Insurance (PPLI)

Although a relatively new concept to wealth advisory firms outside of the US, PPLI has been an effective tool for 40+ years as a robust planning tool for HNW families. Since most offshore company and Trust structures are porous at best nowadays, the combination of PPLI has the ability to reinforce legacy structures and planning to meet the constantly changing fiscal and regulatory landscape challenges of today. It returns privacy to families, provides tax deferral, facilitates intergenerational wealth transfer and secures protection on a myriad of assets, from cash, stocks, PE, jets, yachts, art, hedge funds and also digital assets.

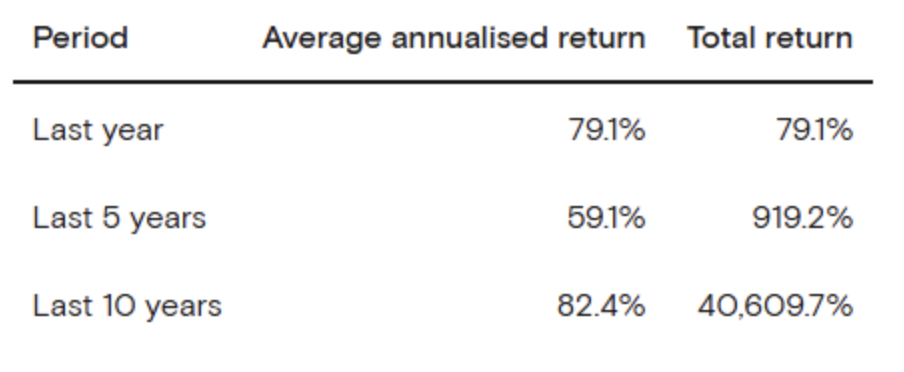

Digital Assets – Story of Bitcoin (BTC)

Since its inception in 2009, Bitcoin has experienced unprecedented price appreciation, including an average annual return of 74.1% over the last ten years. Between 2012 and 2025, the Bitcoin index demonstrated a positive annual return in nine of the 13 years (99%) with a total return over the last 10 years of 25,480%. While underscoring that past performance is no indication of future returns, the most vocal advocates of Bitcoin believe that its fixed supply of 21 million coins makes it a compelling store-of-value, an ideal hedge against the debasement of government-issued fiat currencies.

Source Bitcoin: historical performance from 2011 to 2025

Regardless of the volatility associated with this asset class, avid proponents of Bitcoin firmly believe that its decentralized nature is the purest definition of an asset that provides an effective hedge against the deleterious effects of inflation – a form of “digitized gold” with exceptional upside potential over the long term.

Combining PPLI and digital assets allows HNWIs to participate in this asset’s appreciation potential over a longer time horizon, while mitigating some of the risks associated with direct ownership. PPLI is uniquely positioned as a compelling wealth management solution for tax, asset protection and risk mitigation. Moreover, when PPLI is combined with a properly-structured trust, the beneficiaries of the trust can receive a tax-free disbursement of the PPLI’s underlying assets, thereby optimizing the intergenerational wealth passed on to the insured’s heirs. It is widely accepted that digital assets are the norm in the HNW portfolio.

PPLI – Overview

There are multiple jurisdictions for PPLI and it is important to source the correct one(s) to meet the needs today and for the future ensuring alignment with the priorities of the family. Tax optimization is key and assessing the number of dual or double taxation agreements (DTA) will allow the PPLI to deliver exceptional returns unhampered by income and/or capital gains. Similarly, the platform can be Sharia compliant for families seeking a solution in line with their religious beliefs (Murabaha/Wakalah).

Investment gains within the policy grow on a tax-deferred basis, meaning they are not subject to capital gains tax as long as they remain within the policy. Similarly, death benefit proceeds are typically paid tax-free to beneficiaries, providing a significant advantage in estate planning. This deferral can lead to substantial wealth accumulation over time, particularly for investments with high growth potential. Loans can be taken from a PPLI which may be tax advantageous as opposed to a distribution should the need for liquidity arise. Moreover, credit committees of Banks/Finance firms have greater comfort lending to insurance companies (the PPLI Provider) since the structure is robust, domiciled in a recognised and regulated jurisdiction, can deploy loan protection cover and is easy to collapse if needed and/or in case of default. PPLI can combine multiple assets within one platform so there is no need to have one for digital assets and another for more conventional forms of investment. Some PPLI are designed to be country specific providing bespoke benefits tied to the approval of the tax authorities concerned.

The misconception that digital assets are somehow outside the purview of governmental bodies is diminishing and misguided at best. The very nature of the blockchain is to track every transaction. The ownership of digital assets can be kept private, within the PPLI structure, providing an additional layer from public disclosure, asset protection and succession. This is particularly important for individuals who value discretion in their financial affairs, especially when digital assets attract enhanced scrutiny and regulatory oversight at present. This will subside over time as growing acceptance of digital assets as part of a diversified investment strategy continues to become mainstream.

How to use Digital Assets with PPLI

The process to onboard digital assets is relatively straightforward and initially, as with all AML/KYC procedures, the provenance of the assets requires pre-screening. This screening is possible with a number of block chains with associated digital assets held within the client’s wallet.

Each PPLI policy is linked to a dedicated sub-account at the custodian, ensuring transparency and ownership separation. Moreover, as is the case in all asset classes, there is never any contamination of assets between that of the client and the PPLI provider. This gives clients further comfort that their assets do not sit on the balance sheet of the PPLI company which is not the case with the likes of Banks.

Once compliance screening complete, all assets are received directly from client wallets, so there is no need to liquidate; sometimes referred to as in specie transfer. Thereafter, the client can create multi-user approval flows with role-specific permissions (initiator, approver, auditor, admin) as part of the design of the PPLI solution. Similarly, the various methods of managing digital assets remain in terms of staking, option strategies, loans, HODL, on/off ramp to fiat and the use of third-party managers.

Combine these options with the aforementioned benefits coupled to distinct beneficiary designation from outset (changeable as required) it provides a compelling platform to effectively manage all assets, not just digital ones. So many digital asset investors have no mechanism for ensuring assets are passed in a timely manner with regulated oversight to ensure their wishes are executed privately, tax efficiently and without probate. Some beneficiaries have no idea of the digital assets to which they could be entitled which means they can be lost to the ether from which they came.

PPLI on the HNW Client Agenda

The ubiquitous traditional offering from HNW advisory in terms of digital assets is stale and no longer as effective with a NextGen consumer that demands innovation. It is clear that there are major benefits to be attained with PPLI beyond the digital asset headline of potentially huge returns over the long term. Without careful planning, a well-intended digital asset portfolio can fall foul to adverse taxation, lack of regulated third party oversight without a clear path for inter-generational wealth transfer. For HNW families who value their privacy, seek tax deferred growth and the confidence to access this exciting asset class, PPLI can no longer be overlooked in the international wealth planning arena.

Tim Searle TEP

Tim has been offshore for nearly 30 years, lives in Dubai, full STEP member, Worshipful Company of Tax Advisers and a qualified CII (Chartered Insurance Institute of London). He is frequently asked to speak at conferences, radio and writes for various publications. He sold his former company to a FTSE Listed PLC and now provides bespoke advisory to HNW clients globally. He is married with four children and a former Naval Officer.

Tim Searle – Leaders List Profile