Inheritance Tax: Combining Trusts with Insurance Solutions

Inheritance Tax (IHT) has taken centre stage in the UK political agenda whether you are a farmer, non-domicile or those who just think it is unfair. Article by Tim Searle.

Historically, it has been around in various forms since 1694, to fund the war against Napoleon in 1796, referred to as estate duty in 1894, then labelled from Capital Transfer Tax to IHT in 1986 as we know it today. Roy Jenkins MP famously quoted that IHT is paid by those that distrust their heirs more than they dislike HMRC. Which, even with only 4% of British estates paying IHT, that quote continues to ring true.

The UK Government has and continues to increase taxes on UK property and anti-avoidance measures aimed at offshore structures. These include ATED (Annual Tax on Enveloped Dwellings), ROE (Register of Overseas Entities), NRCGT (Non Resident Capital Gains Tax), supplementary SDLT (Stamp Duty Land Tax) for overseas buyers, to name but a few and most designed to increase revenue for the UK Government.

HMRC’s retroactive changes in 2017, brought most UK property assets under the scope of IHT regardless of the Trust structure, offshore company, nationality, domicile, residence or passport. This was very much on the heels of the Paradise/Pandora/Panama Papers where Governments actively increased the exchange of information and the ability to see through to the UBO (Ultimate Beneficial Owner). This was further bolstered by other multi-jurisdictional implementations of CRS (Common Reporting Standards) and FATCA (Foreign Account Tax Compliance Act). These initiatives had a veiled intention of enhancing AML/KYC but in essence were tools for Governments, collaboratively, to collect more tax. As a result, the IHT haul has increased 20%+ year on year since the implementation of this change.

Since only 4% of British nationals are paying IHT (94 reliefs, allowances and exemptions to mitigate exposure with careful planning), it would seem someone else is picking up the tab. Most British nationals misunderstand IHT so there is little chance foreign nationals have; it is no surprise that they are falling foul and paying the price.

UK situs assets are those that have a title of ownership in the UK which can include bank accounts, shares, investment portfolios, art, classic and supercars, watches, jewellery; the list goes on. This article will focus on residential property alone since this is likely to be the most valuable of all UK assets and how these rules affect foreign owners of said property.

Pre 2017, the most effective method to purchase residential property in the UK was by way of an offshore company and trust which managed not only IHT but capital gains tax too. This fuelled the offshore Trust, Legal and Fiduciary (Advisory) industry for many years with jurisdictions like the BVI, Jersey and Guernsey being some of the main benefactors. Foreign buyers would be offered a raft of structures, and structures within structures, to mitigate the various taxes associated with UK property ownership. Some of these structures were designed to obfuscate reporting, conceal the UBO and obviate the tax liability.

The new rules imposed in 2017 mean that these structures are ineffectual from shielding foreign owners from IHT. It also simplifies the planning options open to advisors and their clients. Simply, the options to protect assets are as follows:-

Sell

Dispose of the property, take the proceeds offshore, survive 2 years and there is no further exposure to IHT.

Gift

By passing the asset to another person, normally a family member, surviving 7 years, will not trigger any IHT when the person gifting dies. That said, the person receiving the gift, typically a younger person, now has the liability. It should be noted that the owner can no longer benefit from the property and the person receiving the gift has full control to do with the asset as they wish. For many patriarchal families, for this reason they do not like giving up control of the asset to a younger member of the family for fear of squandering. So, if retaining the asset (and control) the property will eventually be liable to 40% tax.

Insure

An insurance structure will pay the IHT liability when, not if, it falls due. It allows full control/access throughout, creates the liquidity to meet the IHT bill in a timely manner, remains outside of probate/Shariah complexity, in most instances will be cheaper than paying the full eventual liability and allows the value to pass to the family swiftly. Insurance benefits can be paid to the Trust providing the liquidity to satisfy HMRC and settle debt.

It is worth noting that on death, the property passes to the control of HMRC who will not release until IHT is settled within 6 months. The property cannot be sold or passed to family members until this liability has been settled in cash. More importantly, failure to meet this deadline can result in the asset being fire sold or worse, confiscated.

Insurance remains the cornerstone to any robust estate or tax efficient planning structure but became mostly overlooked running up to 2017. Insuring against this inevitable tax is the most effective way to retain control and ensure the liquidity is in place to meet the tax bill. However, it is overlooked by Advisory mainly because of their lack of expertise of insurance solutions, access to offshore insurers, understanding the permutations of insurance from an array of overseas jurisdictions. Most UK based insurance solutions are not available to foreign nationals, so this amplifies the problem further. The foreign owner seeking advisory in the UK, on UK situs when the solution could be outside of the UK, compounds their dilemma. Certainly, there are better IHT insurance solutions available internationally than in the UK which this profile of client has access (if they knew). Here are some examples:

Insurance creates immediate cash, outside of UK probate allowing families to face these challenges with confidence. It makes financial sense to pass this inevitable risk to a major insurance company rather than locking up capital to meet the eventual liability. Notwithstanding, since the IHT bill increases in line with the value of the asset, so offsetting this future risk to an insurance company for a fraction of the IHT liability at today’s property value makes financial sense. As with all insurance, the best time to buy it is yesterday so the permutations should be explored the sooner the better.

Some Advisory think insurance is expensive, thinking only of the premium required today and not what it is offsetting in future. Few Advisory realise that offshore solutions can cost nothing with the options of premiums being recouped in full at a point in future. This is particularly useful should the property be sold in future, whereby the policy can be surrendered, premiums returned, ergo, the solution can cost nothing.

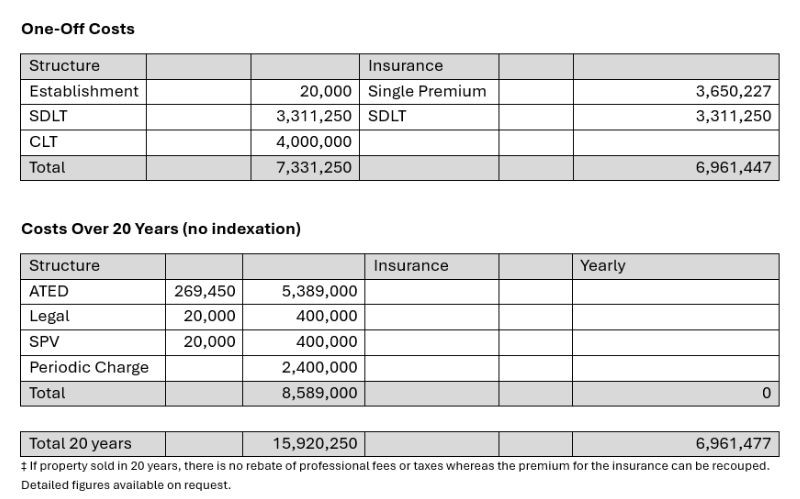

When discussing costs, the revised rules have impacted the financial suitability of holding property in structures and should be reviewed if purely to mitigate IHT. Here is a simple table of fees to demonstrate based on the purchase of £20m property with £8m IHT liability.

It is worth noting that mortgages/debts have to be settled on death so insurance can be a mechanism not only to meet the IHT bill but settle the outstanding debt(s) so the asset passes clean and clear to the family as was intended. Insurance works in combination with the Trust so liquidity is created at a crucial period to settle HMRC, clear debts, create legacy and create cash to provide the family with peace of mind.

The rules have changed for foreign investors, most of whom remain unaware of their exposure or the options open to them. Clearly, a blend of onshore and offshore Advisory is needed if value can be delivered to foreign property owners if they are going to be able to protect their assets effectively and efficiently with the onus of ensuring these assets are passed to the future generations in a timely manner considering the impact of IHT.

More education and awareness are needed for both Advisory and foreign investors in this sector if effective planning solutions are to be achieved and reflect the major changes of 2017. Trusts have a fiduciary duty to protect assets for future generations since it’s inevitable a family member will pass. Combining Trusts with Insurance, revisiting existing planning and keeping clients informed will secure favourable outcomes for all parties and protect the assets of the families we serve.

Tim Searle’s Citywealth Leaders List Profile

HNWTAX’s Citywealth Leaders List Profile

Subscribe to the Citywealth Weekly Newsletter to learn more about Private Wealth Management.

Read more:

Navigating a hard market: Fresh insurance strategies for the Ultra-Wealthy

Property and life insurance: issues for UHNWIs

OBBBA and the Global Wealth Shift: What Private Client Advisors Must Know Now

What Is OBBBA and Why It Matters for Global Wealth.

Turning Passion into Legacy: The Smart Way to Donate and Invest in Art

Art has increasingly come to be seen not only as a source of personal enjoyment but as a meaningful component of financial and estate planning.