Cash is not always king

Wealth Manager at MASECO Alex Dolton discusses why, in the current economy, cash may not always be king.

Towards the end of December 2021 and beginning of 2022 inflation around the world started to rise quickly and central banks increased interest rates to try and tame the rise in prices. The increase in interest rates meant the return you could receive on cash savings became more attractive, something we haven’t seen since 2009 in the UK (and slightly earlier in the US). Many investors were left asking whether it is worth switching into cash and putting excess cash into the bank instead of investing. The lure of cash was even more tempting especially after the falls in both equities and fixed income in 2022. Many clients were asking ‘why take the risk investing in financial markets when you can achieve around 5% putting your cash in the bank?’ Below we unpack why we believe cash is not always king.

The interest earned from cash is still negative in real terms

Even with interest rates rising to levels not seen in well over a decade, the cash returns when inflation is factored in have mostly been negative. Whilst for some there is comfort knowing that you will receive a nominal amount at the end of the term, when you factor in the current levels of inflation, your money is not maintaining its purchasing power over time. There may be short periods of time when cash will outperform inflation but when you start stretching the timeframe, holding large portions of your wealth in cash is likely to underperform inflation the longer the timeframe.

Why not just switch into cash, avoid market drawdowns and then reinvest when markets calm?

Over the past few years macroeconomic uncertainty has remained high and financial markets have remained volatile. Many investors have therefore thought about seizing the opportunity to switch out of equities and bonds and hold cash to earn a higher return and redeploy when markets stabilise. However, forecasting the future is incredibly difficult to do and one of the main reasons we encourage our clients to avoid this approach. Recently we have witnessed inflation fall quite quickly in both the US and UK and whilst in theory you could allocate capital into a fixed term cash product whether that be a bond or a certificate of deposit to lock in the higher interest rate, during that period other asset classes might have started to rebound and you will miss out on positive market performance.* Timing this is very difficult to do.

*Remember if you have cross border tax reporting requirements, fixed term cash products such as bonds might be subject to tax on a gain made from any foreign exchange movement.

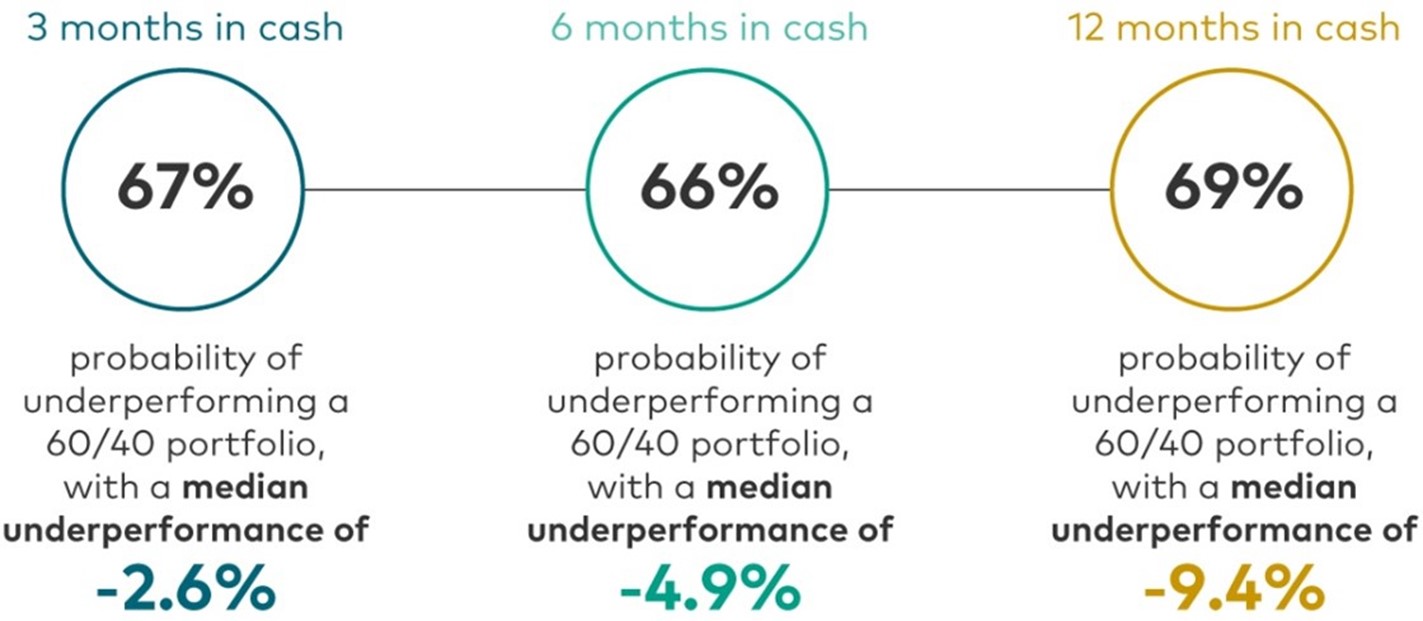

Time in the market not timing the market

Timing the switch out of cash as interest rates start to fall and into a diversified multi-asset portfolio is extremely difficult to get right and is likely a sure-fire way to destroy wealth quickly. Vanguard compares the impact of staying in cash for 12 months versus a 60/40 portfolio over different time periods between January 1990 and March 2023. As you can see, by staying in cash for 12 months there is nearly a 70% probability of underperforming a 60/40 portfolio.

Past performance is not a reliable indicator of future results.

Notes: The chart shows the distribution of excess returns of cash over a global 60% share/40% bond portfolio in a 3-, 6-, and 12-month period after 3-month total returns of global shares were below 5%. Global shares represented by the MSCI AC World Total Return Index. Hedged global bonds represented by the Bloomberg Global Aggregate Bond Index Sterling Hedged index. Cash is represented by sterling 3-month deposit rates.

Source: Vanguard calculations in British pounds, based on data from Refinitiv. Data is based on the period between 31 January 1990 and 31 March 2023.

What should I do?

It is important to remember that cash is not necessarily a risk-free asset. Before considering switching to cash, it is important to take a step back and remind oneself of the goals associated with your investments. Over long investment time horizons stocks and bonds have historically been a much better inflation hedge. This is because investors are rewarded for taking additional risk. There will be periods where the interest received on cash will be above the current rate of inflation but this can quickly change and create an opportunity cost.

Taking advantage of the higher interest rates for your emergency cash reserves or known near term liabilities is a must but holding too much in cash that could be invested in a diversified investment portfolio for the long term is likely to reduce the probability of your wealth maintaining pace against inflation.

The importance of retirement planning for female investors

Mind the pension gap! Wealth Manager at MASECO Private Wealth Emma James discusses the daunting task of financial planning for the future and its importance, especially for women.